The current commercial real estate crisis is a pressing concern that has arisen from the fallout of the pandemic and subsequent economic shifts. With office vacancy rates soaring across major cities, we face a significant challenge in the real estate market that could jeopardize financial stability. As businesses grapple with the impact of hybrid work cultures, the demand for commercial spaces has plummeted, resulting in depressed property values. This strain, exacerbated by rising interest rates and looming bank failures, raises alarm bells about the potential for widespread economic repercussions. The intricate relationship between these factors highlights the urgent need for strategies to navigate the complexities of this crisis.

In light of the ongoing struggles in the office property sector, this situation could also be described as a commercial property debt dilemma. The excessive vacancies and declining demand for workspaces have created a domino effect, influencing related aspects of the financial landscape. With office space providers facing expanding challenges, the ripple effects on the banking sector and broader economy cannot be overlooked. Financial professionals are increasingly monitoring the risk of economic fallout due to potential bank failures linked to unrecoverable commercial property loans. These dynamics call for a robust discussion on the sustainability of investments in a shifting real estate landscape.

The Economic Impact of High Office Vacancy Rates

High office vacancy rates have emerged as a significant concern in the current real estate market, primarily driven by the pandemic’s long-lasting impact on work habits. As businesses have embraced remote and hybrid models, demand for downtown office spaces has dramatically dwindled, with vacancy rates soaring between 12% and 23% in major cities like Boston. This downturn has led to a decrease in property values, prompting worries among financial experts about the potential ripple effects on the broader economy. As these buildings remain unoccupied, landlords are facing increased financial stress, which could potentially translate into slower economic growth as businesses scale back their operations.

Moreover, the economic implications of these high vacancy rates extend beyond just the real estate market. Many banks and financial institutions have significant exposure to commercial real estate loans, which may lead to distress if office buildings continue to underperform. This concern is compounded by the looming deadlines for outstanding property loans that are now due, leading to fears that widespread delinquencies could directly impact the banking system. If can’t adjust quickly to the high vacancy landscape, there could be severe repercussions for local economies as businesses struggle to stay afloat amidst declining property values.

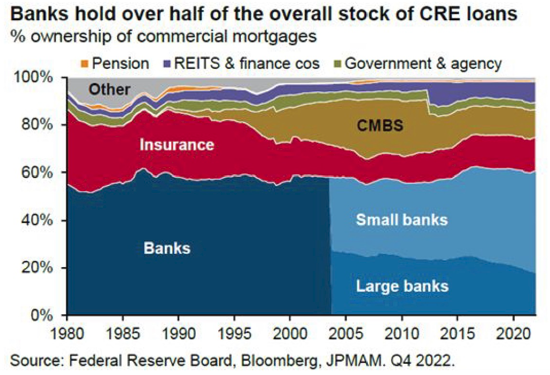

Potential Consequences of the Commercial Real Estate Crisis

The commercial real estate crisis, exacerbated by rising interest rates and a significant volume of maturing loans, poses a threat to the stability of financial institutions in the U.S. Kenneth Rogoff, an economist, outlines that while no widespread financial meltdown is expected, the potential for significant bank failures, especially among smaller institutions, remains. With many banks heavily invested in commercial property, any substantial distress in this sector could lead to forced consolidations or bailouts, reminiscent of past financial crises. Such a scenario raises alarms about the interconnectedness of the banking sector and the real estate market, indicating that troubles in commercial real estate could trigger broader economic challenges.

As regional banks face mounting pressure, the likelihood of bank failures surfaces as a critical concern. These institutions, often less diversified than their larger counterparts, have shown vulnerability to market shifts and are subject to more significant risks associated with high office vacancy rates. The impact of this potential crisis could extend beyond just the banks; it may lead to an inability for consumers to secure loans, hampering economic growth and decreasing overall consumer confidence. Thus, understanding and addressing the commercial real estate crisis becomes paramount to ensuring the overall stability of the economy.

The Role of Interest Rates in the Commercial Real Estate Market

Interest rates play a critical role in shaping the landscape of the commercial real estate market. When interest rates were historically low, many investors took on excessive debt, confident that these rates would remain favorable indefinitely. However, the rapid rise in interest rates has altered this balance, leaving many real estate investments precariously over-leveraged and at risk of default. Coupled with the pandemic-induced rise in office vacancy rates, the pressure on property owners has intensified, leading to speculation about the future viability of many commercial ventures.

The Federal Reserve’s stance on maintaining higher interest rates has further compounded the complexity of the situation. Investors, particularly in the commercial sector, are now grappling with uncertainty, as the cost of borrowing has significantly increased. Many look towards potential economic downturns to create opportunities for a shift back to lower rates. However, as interest rates remain elevated, the fear of rising delinquencies among commercial loans heightens, underscoring the need for strategic planning and adaptation within the sector. This dilemma emphasizes how vital interest rates are to sustaining a healthy commercial real estate market.

Strategies to Navigate the Real Estate Downturn

Addressing the ongoing challenges in the commercial real estate market requires innovative strategies and a willingness to adapt. One potential solution is to facilitate conversions of vacant office spaces into more viable commercial uses, such as residential apartments. However, as many industry experts highlight, zoning regulations and structural limitations often complicate these conversions, making them less feasible than they appear. Therefore, a collaborative approach involving policymakers, urban planners, and real estate stakeholders is essential to navigate the intricate challenges posed by high vacancy rates.

Additionally, stakeholders may explore refinancing opportunities to alleviate some financial burdens associated with maturing loans. If long-term interest rates were to decline significantly, it could enable property owners to refinance at more manageable rates, potentially stabilizing the market. Proactive measures, including improved property management and strategic investments in renovations, may help reposition assets to be more attractive to tenants. Ultimately, a multifaceted strategy that considers prevailing economic conditions is crucial to mitigate the impact of the commercial real estate crisis.

Leveraging Technology in Real Estate Recovery

As the commercial real estate sector navigates this challenging landscape, leveraging technology emerges as a critical element of recovery. The integration of advanced analytics and real estate tech platforms can provide insights into changing market dynamics, ultimately enabling property owners to make informed decisions about pricing and leasing strategies. This digital transformation can also include virtual tours and enhanced marketing techniques that attract potential tenants in a market that is shifting toward remote engagement.

Moreover, technology can streamline property management processes, ensuring that vacant spaces are maintained efficiently while attracting new tenants. Building owners can utilize data analytics to identify which amenities or services resonate most with prospective tenants, helping to position their properties more competitively in the marketplace. By prioritizing innovation through technology-driven solutions, the commercial real estate market can not only recover but also emerge stronger and more resilient in the face of ongoing economic challenges.

Impact of Bank Failures on Regional Economies

The potential for bank failures in the wake of the commercial real estate crisis could trigger significant repercussions for regional economies. As many local and regional banks have a concentrated investment in commercial properties, their struggle to withstand financial pressures may limit credit availability for businesses and consumers alike. This restricted access to capital can hinder economic growth, reduce consumer spending, and ultimately impact job creation, leading to a potential downturn in regional economic health.

Moreover, the fallout from bank failures can create a ripple effect, affecting local businesses’ confidence and investment decisions. As communities witness banks unable to fulfill loan commitments, the perception of financial risk can lead to hesitation among entrepreneurs to launch new ventures or expand existing businesses. This hesitation may slow down the overall economic recovery process, emphasizing the need for robust oversight and support mechanisms within the banking sector to mitigate these threats.

The Future of Office Spaces in a Changing Market

The future of office spaces in the wake of shifting work models is uncertain yet ripe with possibilities for transformation. As the demand for traditional office environments continues to decline, there is growing interest in redesigning these spaces to accommodate a more flexible workforce. This could include creating multi-functional spaces that support collaborative work while also allowing for individual privacy—an essential consideration in our evolving employment landscape.

Furthermore, as businesses become increasingly attuned to the preferences of their employees, the need for amenities that improve workplace satisfaction, like health and wellness features, will be paramount. Such innovative adaptations not only enhance the attractiveness of office properties but potentially also stabilize earnings for landlords dealing with high vacancy rates. Embracing this cultural shift in workplace expectations could determine the success of future office ventures by aligning real estate offerings with the evolving needs of the workforce.

Consumer Responses to the Commercial Real Estate Landscape

In light of the commercial real estate challenges, consumer behavior is also expected to shift as individuals navigate uncertain economic conditions. With potential disruptions in regional banks influencing lending availability, many consumers may adopt a more cautious approach to spending and investment. This heightened awareness can impact consumer confidence, causing individuals to reassess their financial commitments and prioritize saving over expenditure amid fears of a looming economic downturn.

Additionally, shifts in the demand for commercial spaces may lead consumers to seek alternatives to traditional office environments, such as co-working spaces or hybrid models that promote flexibility. This adaptation reflects a broader trend of consumers prioritizing personal well-being and quality of life in their professional choices. Consequently, businesses will need to remain agile and attuned to these consumer preferences to stay relevant in a rapidly changing landscape, directly influencing occupancy rates and overall economic dynamics.

Mitigating Risks in the Real Estate Sector

To effectively mitigate the risks associated with the ongoing commercial real estate crisis, stakeholders must embrace proactive risk management strategies. This includes assessing the potential exposures within their portfolios and recalibrating their investment strategies to prioritize resilience in the face of continued uncertainty. Financial institutions should conduct thorough due diligence on their commercial real estate holdings and consider diversifying their investments to buffer against potential downturns in the sector.

Furthermore, collaboration between real estate developers, financial institutions, and policymakers can enhance risk mitigation efforts by fostering innovative solutions that address issues such as high office vacancies and declining property values. By working together to craft flexible regulations that can adapt to changing market demands, stakeholders can create a more sustainable real estate environment that empowers both businesses and consumers while ensuring that the risks of commercial real estate investments are effectively managed.

Frequently Asked Questions

How are high office vacancy rates contributing to the commercial real estate crisis?

High office vacancy rates are a critical factor in the commercial real estate crisis, as they lead to depressed property values. The surge in remote and hybrid work arrangements since the pandemic has reduced demand for office space, causing vacancy rates in major U.S. cities to soar between 12% and 23%. This oversupply results in significant financial strain for investors, leading to potential losses and affecting the overall real estate market.

What economic impact can the commercial real estate crisis have on the U.S. economy?

The commercial real estate crisis has the potential to create a ripple effect throughout the U.S. economy. High vacancy rates and declining property values can lead to losses for regional banks heavily invested in commercial real estate loans. This can result in stricter lending terms and decreased consumer spending, which may slow economic growth, even amidst a generally strong job market.

Why are experts concerned about bank failures linked to the commercial real estate crisis?

Experts express concerns about potential bank failures connected to the commercial real estate crisis due to the high volume of loans coming due. With approximately 20% of the $4.7 trillion in commercial mortgage debt maturing this year, significant delinquencies could jeopardize the stability of regional banks that hold a substantial amount of this debt, possibly leading to bankruptcies and further economic turmoil.

How do rising interest rates affect the commercial real estate crisis?

Rising interest rates exacerbate the commercial real estate crisis by increasing borrowing costs for investors who had previously over-leveraged their investments during a period of low rates. Higher interest rates lead to reduced refinancing opportunities and make it more difficult for struggling properties to recover, thus intensifying vacancy issues and diminishing property values in the real estate market.

Can the commercial real estate crisis affect consumers directly?

Yes, the commercial real estate crisis can impact consumers directly. Losses incurred by regional banks due to failed commercial real estate loans can result in tighter credit availability and stricter loan terms for consumers. Additionally, pensions tied to these real estate investments may also suffer losses, affecting retirees’ financial stability in the long run.

What measures could be taken to mitigate the ongoing commercial real estate crisis?

To mitigate the commercial real estate crisis, strategies could include stabilizing long-term interest rates to facilitate refinancing opportunities for distressed properties. Additionally, incentive programs for converting unused office spaces into residential units could help alleviate excess supply. However, significant adjustments and potential bankruptcies are inevitable within the current economic landscape.

What is the current outlook for the commercial real estate loan market?

The outlook for the commercial real estate loan market is uncertain. While large banks may be better positioned to absorb losses due to diversification, regional banks that focus on commercial real estate loans could face considerable challenges as delinquencies rise. This precarious situation underscores the importance of monitoring market trends and potential regulatory responses to ensure broader financial stability.

Are commercial real estate investors optimistic about future recovery?

Some commercial real estate investors remain optimistic about future recovery, believing that interest rates will eventually decline, providing relief and recovering property values. This optimism is encapsulated in the phrase ‘Stay alive till ’25,’ reflecting hopes for a positive turnaround as the market adjusts to post-pandemic realities.

| Key Issues | Details |

|---|---|

| Potential Economic Impact | High office vacancy rates may lead to significant losses in commercial real estate, impacting banks and the broader economy. |

| Current Vacancy Rates | Boston and major U.S. cities have vacancy rates ranging from 12% to 23%, reducing property values. |

| Surge of Debt | 20% of $4.7 trillion in commercial mortgage debt is due this year, posing risks to banks’ financial health. |

| Regulatory Environment | Large banks are better regulated but regional banks may face greater risks from commercial real estate. |

| Long-term Expectations | Investors hope for a decline in long-term interest rates to improve refinancing opportunities. |

| Broader Economic Context | Despite challenges, the overall economy remains robust with a solid job market and strong stock performance. |

Summary

The commercial real estate crisis poses significant challenges, particularly linked to high office vacancy rates and a wave of commercial mortgage debt coming due within the next two years. While the immediate effects might not lead to a complete economic collapse, the vulnerability of regional banks, alongside the ongoing adjustments in the commercial real estate market, signals potential financial difficulties ahead. As heightened interest rates continue to affect the market, the economy’s health will hinge on how these factors unfold in the coming months.